Categories

Loss MitigationPublished March 9, 2026

Short Sales

The Short Sale Process: What Future Buyers Should Know

A short sale occurs when a homeowner sells their property for less than the amount owed on their mortgage, and the lender agrees to accept the reduced payoff to avoid foreclosure. These situations typically arise when a seller experiences financial hardship and can no longer maintain their mortgage payments.

For buyers, short sales can present opportunities to purchase property below market value, but they require patience and understanding of the process.

How the Short Sale Process Works

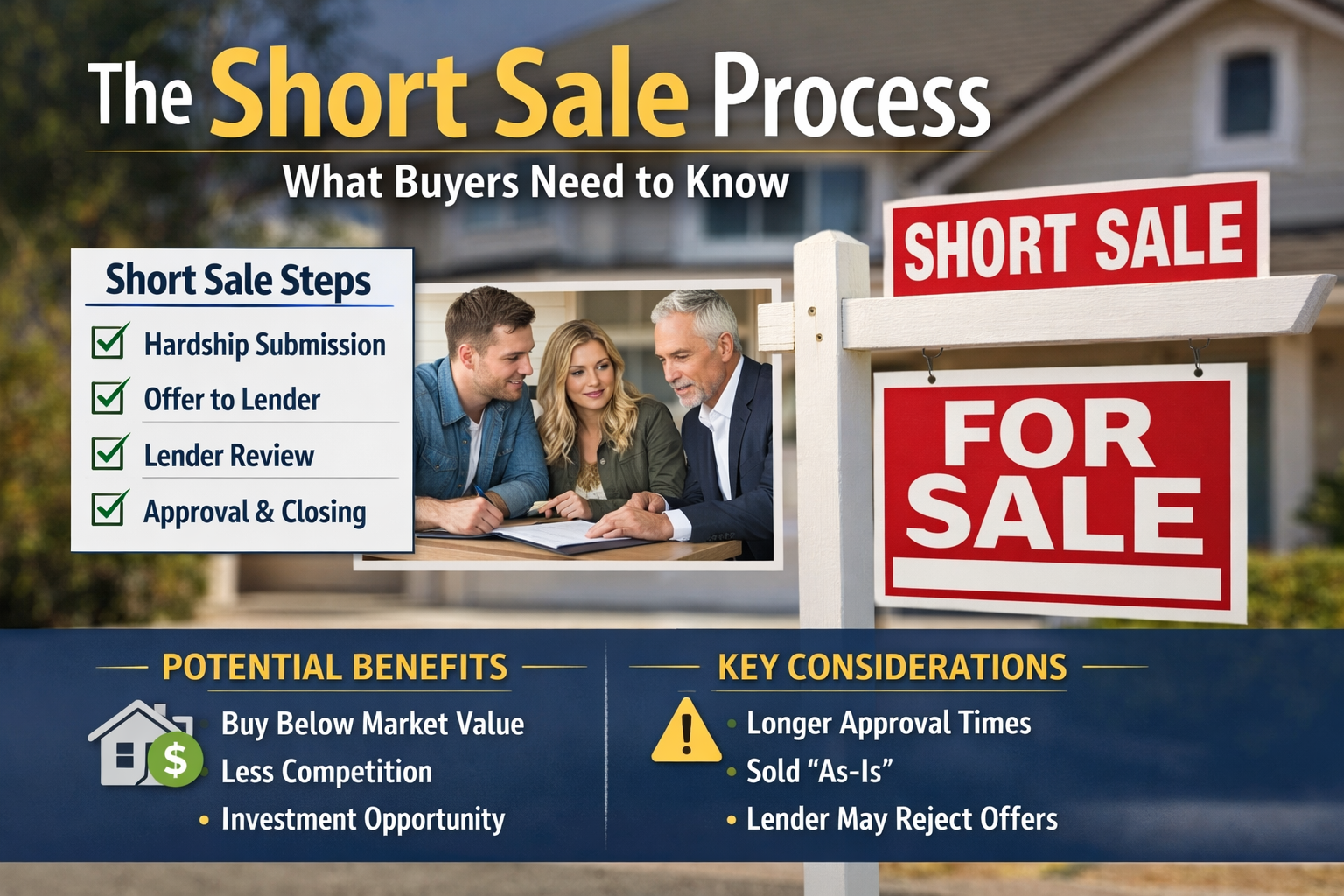

- Seller Submits Hardship Package

The homeowner works with their agent to submit financial documents and a hardship explanation to their lender. - Property Is Listed for Sale

The home is listed on the market and buyers can submit offers just like a traditional listing. - Offer Sent to the Lender

Once a buyer and seller agree on a price, the offer is sent to the lender for approval. - Lender Review

The lender evaluates the offer, reviews the seller’s hardship, and may order a valuation such as a Broker Price Opinion (BPO). - Approval and Closing

If the lender approves the terms, the transaction proceeds to closing similar to a traditional sale.

Timeline

Short sales often take 60–120 days for lender approval, sometimes longer if multiple lenders are involved.

Pros and Considerations for Buyers

Benefits

- Potential to purchase below market value

- Less competition than traditional listings

- Investment or equity opportunity

Considerations

- Longer timelines

- Property often sold as-is

- Lender may reject or counter offers

Final Thought

Short sales require patience, but they can offer strong opportunities for buyers who understand the process and work with an experienced real estate professional. For those willing to navigate the extra steps, a short sale can be a strategic way to purchase property in today’s market.

|

or another way